Up?!? Unlikely

The emerging market currencies are the biggest looser of the slowly unfolding currency war and since the global financial meltdown. The devaluation has been regarded for many as wake-up call to reform their economies.

The officials are already drawing new plans and discarding previous warning policies in order to avoid inflationary pressure and to lure in more foreign investment at a time when global economic output is already slowing. To reverse the downturn, economic decision makers in Mexico, Turkey and South Africa have either intervened, raised interest rates or announced the end of monetary easing.

Morgan Stanley is optimistic about the steps taken by the emerging countries and says it is a good opportunity to turn their economies more competitive. Goldman Sachs Group Inc. predicts further decrease of emerging market currencies.

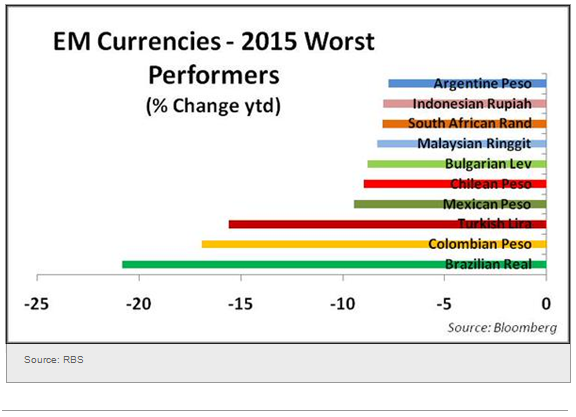

Emerging market worst performers, year to date

The Brazil real, Colombian pesos, Turkish lira are the worst performers year to date and since mid-May the real, ruble, Colombian and Chilean pesos lost 10 more percent from their value. The Hong Kong dollar lost only 0.02 percent, mainly because it is pegged to the U.S. dollar.

Commodity Surplus

On Friday the Russian ruble plunged 3.31 more percent and closed at 61.7050 in New York after an interest-rate cut. The Central Bank of Russia already stopped buying dollar to increase its foreign reserves after a flight that nearly eliminated all its gain this year.

The Thai baht is record weak and fell to a six-year low Friday, while South Africa’s rand closed at 12.6808, the worst level in more than a decade.

It is easy to identify the reasons behind the emerging market currency losses. Interests rates in the U.S. are expected to rise this year attracting investors from everywhere. Simultaneously, the commodity prices that granted quick economic boost to many of the emerging countries are falling.

Many economists and investors expect U.S. interest rate hike this year September, alluded previously by Janet Yellen Fed Chairwoman, in response to the recovering U.S. growth and labor market. Higher U.S. returns would make emerging countries’ asset riskier and less appealing, just like the commodity surplus and the slower Chinese growth.

Boom Times Are Over

“Central banks are trying to preempt a little bit of the currency volatility that could come from when the Fed decides to lift off,” explained in a Bloomberg interview James Lord, Morgan Stanley’s global emerging-market strategist.

Many emerging countries missed their chance to implement structural reforms during the big times to cushion the effect of such decline.

“Commodity-exporting countries are readjusting to the new reality on the fiscal side, but that takes time,” Janne Muta, chief analyst at HotForex, said in an online interview. “Monetary policy has to compensate for the sort of fiscal reforms that weren’t taken when they should’ve been.”

Indonesia and Colombia experiencing near-record current account deficits so the drop in currencies is a “necessary adjustment to address imbalances,” explained Goldman Sachs analyst Kamakshya Trivedi in a report. He forecasts further emerging market currencies devaluation as governments fail to implement structural reforms in the shifting global environment.

The Emerging Market Currencies Contra Foreign Reserves

Many emerging countries had to tap their Fx reserves to reduce currency imbalances

The good news is that emerging countries are sitting on $7.5 trillion in FX reserves, which allows them to fight against chaotic currency drops. Furthermore, most of the emerging currency exchange rates are unpegged so the emerging countries can avoid major meltdowns, told Pablo Cisilino, a money manager at Stone Harbor Investment Partners.

“That’s a long-term fundamental change in emerging markets that should make investors more comfortable about what’s going on, regardless of what happens,” explained the expert.

Bank of Mexico increased its daily dollar sale intervention program by $150 million on Thursday. At the same time, it reduced the minimum price drop required to activate unusual dollar sale intervention to 1 percent, from 1.5 percent now.

Brazil’s Currency Crash

Although Mexico’s central bank kept its benchmark interest rate at 3 percent, the policy makers changed the dates of decision making in order to efficiently counter potential Fed rate hike. Mexico is likely to increase benchmark interest rates in the third quarter.

Brazil’s real lost 21 percent this year and its investment-grade status is in danger after the president Dilma Rousseff abandoned its 2015 primary surplus target 0.15 percent of GDP. Central Bank of Brazil raised the interest rate to 14.25 percent (the highest among key emerging economies) in order to fight inflation and lift investors’ confidence.

African central banks also trying to alleviate the currency selloff. South Africa, Uganda, Angola, Kenya and Ghana have all stiffened monetary policy this year to help scare off inflation.

The Malaysian ringit is at 16-year low and to support it, the monetary policy makers sold foreign-exchange reserves. As result, the Malaysian Foreign Exchange Reserves dropped to $100.5 billion.

Rising inflation rate and slowing GDP growth in Turkey

Turkey’s policy makers left the benchmark interest rate at 7.5 percent after dropping it gradually from 10 percent since last year January. Standard & Poor’s predicts rate hike over the next 18 months from the Central Bank of the Turkish Republic to fight accelerating inflation and further currency devaluation.

The same decision been made in Colombia on Friday leaving the borrowing rate unchanged at 4.5 percent. The decision is surprising amid growing fears of accelerating inflation and because the peso has fallen already 17 percent this year.

According to Morgan Stanley’s Lord, central bankers in emerging markets find it imperative to keep currencies stable regardless the potential economic slowdown from higher borrowing costs.

“Currencies are still very much under pressure, so it wouldn’t surprise me at all to see a little bit more of what we’ve been seeing from other central banks,” explained the economist.